The Hottest VC Trends of 2022: Numbers from 2021

Well, it is that time of the year again: numbers and studies about the VC trends and market in 2021 are now mostly available. Adhering to our tradition, we have read the reports (see list of the reports at the end of this post) and done the heavy lifting for you:

- Picked some interesting notes from 2021 – this post

- Compiled our predictions for 2022 – next post

(BTW, you can also read our year-old analysis of the 2020 numbers and predictions for the year 2021.)

Another record year for Venture Capital

The global VC activity reached new extreme record levels in 2021, supported mainly by positive market sentiment and especially the high valuation multiples of tech stocks.

The last 12 or so years have been a wild ride:

- In March 2009, Nasdaq was below 1.300 points

- In November 2021, Nasdaq hit 16.212,23 points

This 12+ year rally of tech stocks (i.e. Nasdaq went up 1278%) has made an extreme impact on the Venture Capital market.

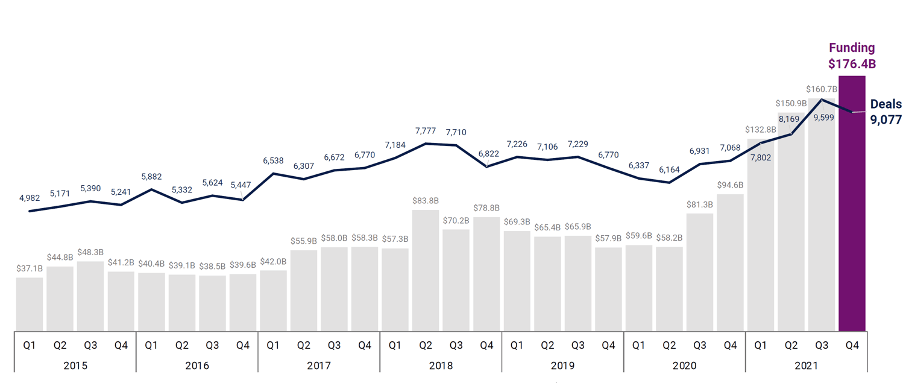

A new all-time high in Global VC activity

111% annual increase to $621B

Source: CB Insight Report Q4 2021

- Global VC funding in 2021 was $621B, more than double the almost $300B in 2020, and ~10x the levels ten years ago

- Q4 2021 was an all-time high quarter with $176B in funding

- Q4 2021 was the sixth consecutive growth quarter (and the fifth consecutive all-time high quarter!)

- Practically all regions saw new record activity levels: the US (as always) was the leading region in dollar volume, followed by Asia and Europe

- But Asia is now the top region for the number of VC deals, with a 36% global deal share

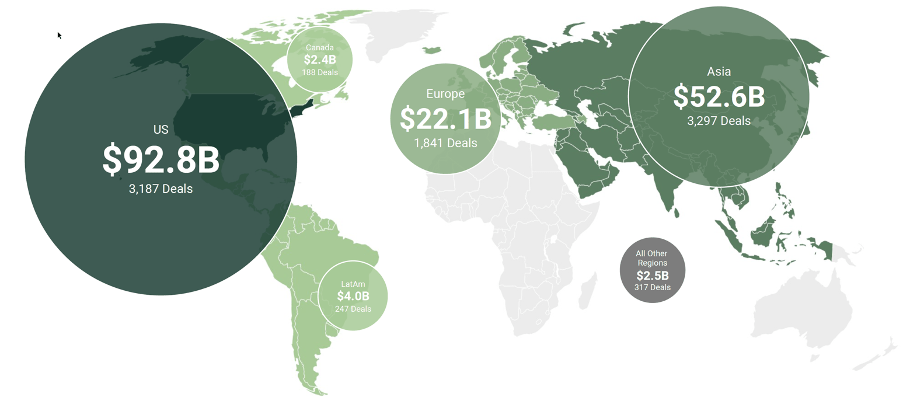

VC activity in Q4 2021

1. Dollars invested: The US volume is larger than Europe and Asia combined

2. Number of deals: Asia had more deals than the US!

Source: CB Insight Report Q4 2021

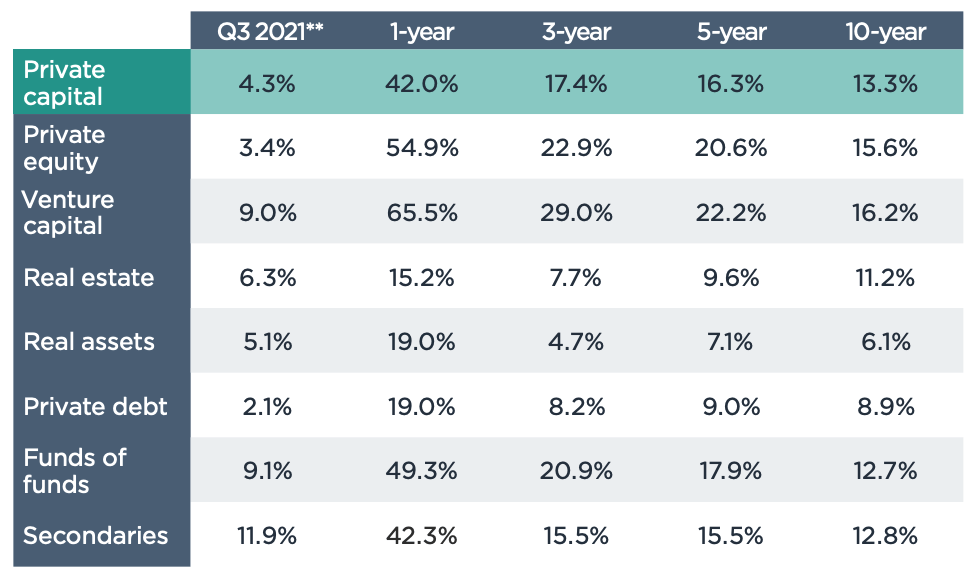

Robust VC Performance

Another dimension of the strong VC scene is the robust performance of VC funds. When compared against other private capital asset classes, Venture Capital outperforms them on all but the very shortest horizons (based on the latest available data as of Q3/2021). Especially notable is how VC outperforms Private Equity on both short and long horizons.

VC outperforms Private Equity on both short and long horizons.

Source: Pitchbook Global Fund Performance Report

Breaking Down The Big Picture

While the year was characterized by fast growth in the overall dollar volume, a more granular look at the market reveals some interesting details, as shown below.

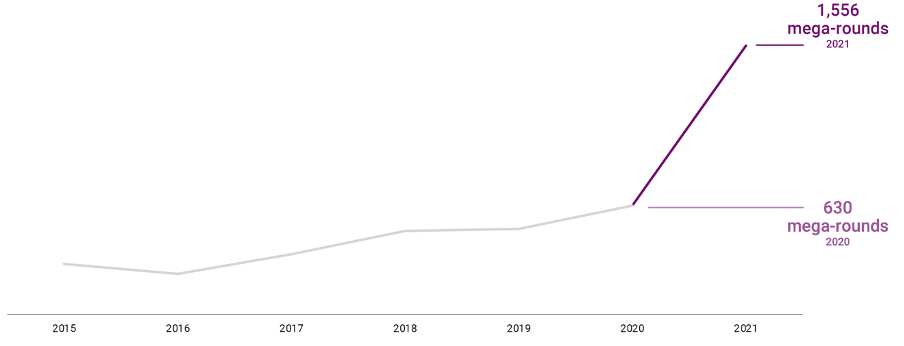

Mega-Rounds

The most significant single phenomenon behind the massive growth of VC funding was the even faster growth of the very large $100M+ mega-rounds. In today’s market, the VC and PE funds provide much of the pre-IPO funding themselves and the late rounds are massive in size.

- The number of global mega-rounds jumped to 1556 deals compared to 630 mega-rounds in 2020

- Mega-rounds represent now 59% of the total funding but only ~5% of the number of deals

A whopping 1556 mega-rounds in 2021, they made 59% of the VC dollars invested

Source: CB Insight Report Q4 2021

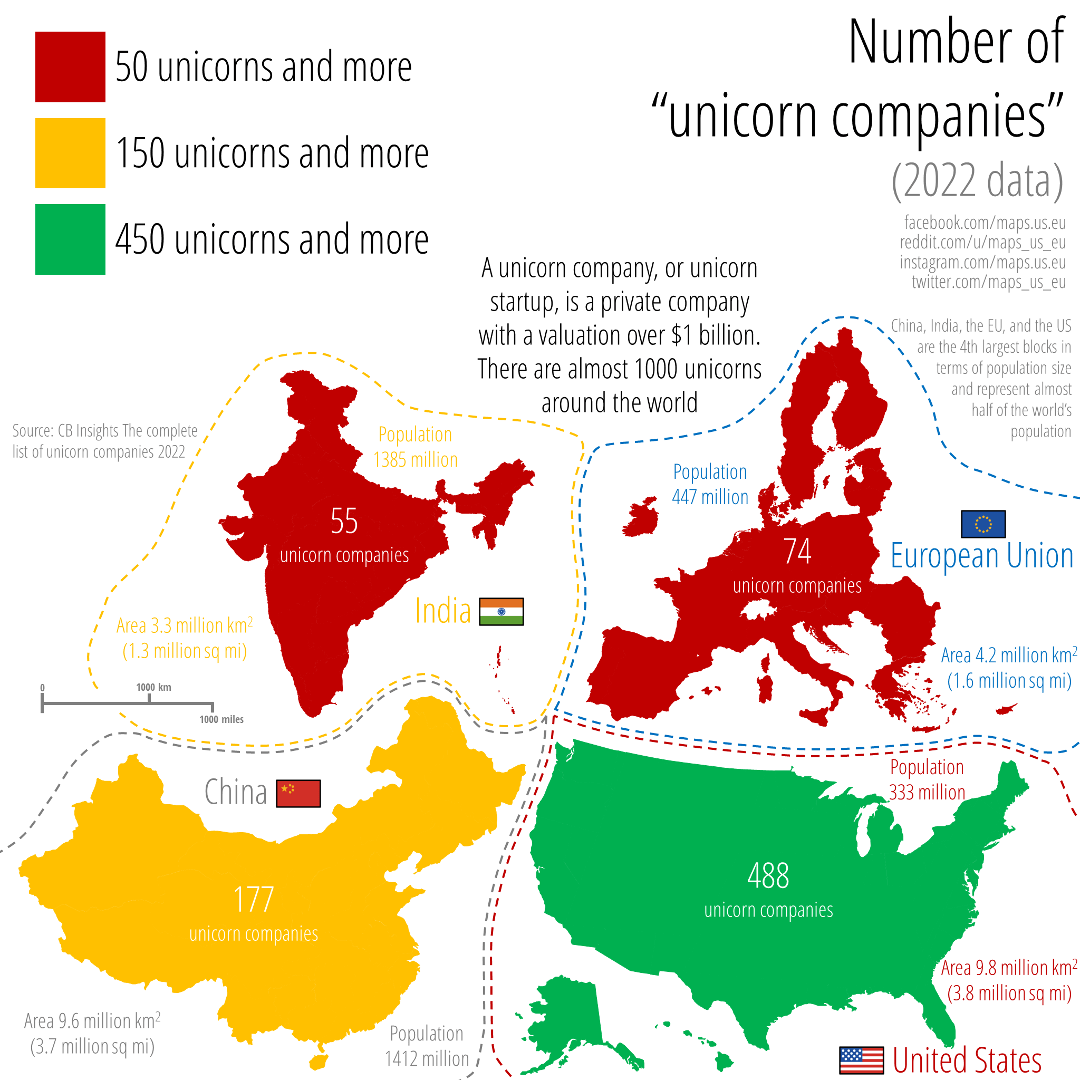

Unicorns

The increase in the number of Unicorns was driven partly by high valuations supported by the peer groups created by the public market. (In some cases, the unicorn valuations have been a bit dubious, as the amount of money invested in those rounds has been smallish and made purely by existing shareholders.)

- The global unicorn count was 959 by the end of 2021, up 69% from the previous year (some sources even cite numbers over 1000)

- 44 companies had decacorn ($10B+) valuations

Countries and areas with the most unicorns

Source: CB Insights & https://www.reddit.com/user/maps_us_eu/

Number of Deals

The number of VC deals has grown relatively steadily on a quarterly basis since early 2020 and was nearing 10,000 deals until the growth stalled in Q4 of 2021. However, there are two interesting data points:

- The number of deals has grown significantly slower than the total dollar amount of the deals. The super active VC market has not inflated the number of deals made, it is more about mega-rounds.

- Europe is showing a strange imbalance: there is a very active early-stage market but only limited follow-on investments in mid-stage.

This European imbalance works in favor of Nexit’s mid-stage technology growth investment strategy: we receive a strong deal flow from early-stage funding recipients combined with somewhat limited competition in mid-stage investments.

Imbalance in Europe: very active early-stage but a fairly passive mid-stage

Source: CB Insight Report Q4 2021

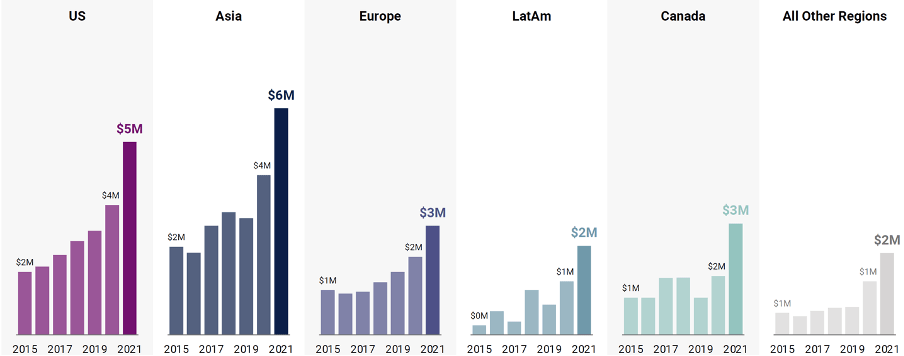

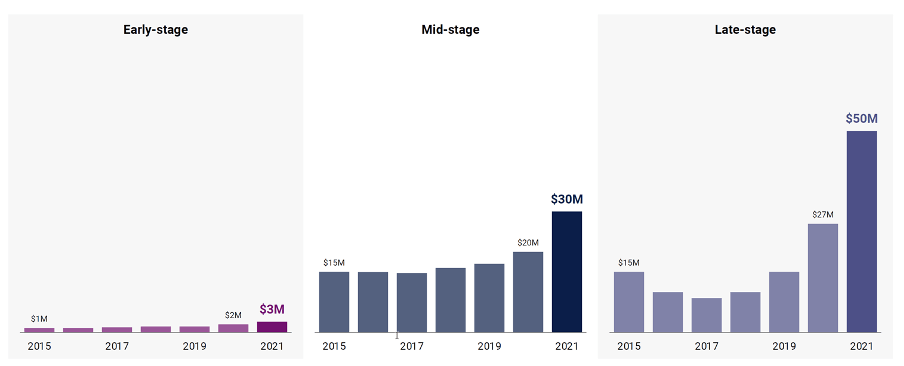

Deal Sizes

The higher valuations, mega-rounds, and unicorns naturally push the average and median deal size up in all regions.

Asia now leads with a $6M median deal size, the US comes in second with $5M, and Europe lags with a substantially smaller median deal size of $3M.

- Both average and median deal sizes reached new all-time highs

- The median deal size went up in all development stages, but the growth was strongest in late-stage deals, where the mean round size nearly doubled

Median VC deal sizes in 2021

1. Asia leading US with $6M, European median is only $3M

2. In late-stage deals, the median deal size nearly doubled

Source: CB Insight Report Q4 2021

The Most Active Sectors: Fintech Leads the Way

Fintech startups raised $132B in funding in 2021 – accounting for 21% of all venture dollars. Fintech funding was up 169% compared to $49B in 2020.

- $1 out of every $5 went to Fintech

- 1 in every four unicorns was in Fintech

Fintech also saw the highest proportion of early-stage deals of any industry, indicating that the sector is ripe for an explosion in 2022 and beyond as startups mature.

Other important active segments include:

- Ongoing digital transformation, especially in Healthcare, B2B services, and Automotive industries

- Cleantech, especially hydrogen-related technologies (see ESG note below)

- Cybersecurity

Artificial intelligence and machine learning continue to dominate as important technology trends but we seem to have passed the AI hype peak, at least for the time being. According to Google Trends, searches for ‘machine learning’ are declining and searches for ‘AI’ have been flat for the past 18 months.

ESG

The importance of ESG (Environmental, Social, and Governance) considerations kept rising in 2021. The consumer pressure towards larger firms to take more action has moved downstream to VC investments, and VC investors are increasing their use of ESG metrics to shape their investment decisions. A further key reason for the emphasis on ESG is the growing importance of ESG stories for companies looking to go public.

The scope of ESG-specific VC investments has also grown, with an increasing focus on net-zero or low emissions technologies across sectors such as food and hydrogen-related investments.

Heading into 2022, there will likely be increasing investments in ESG solutions and tools to help both companies and investors track, measure, and report their results.

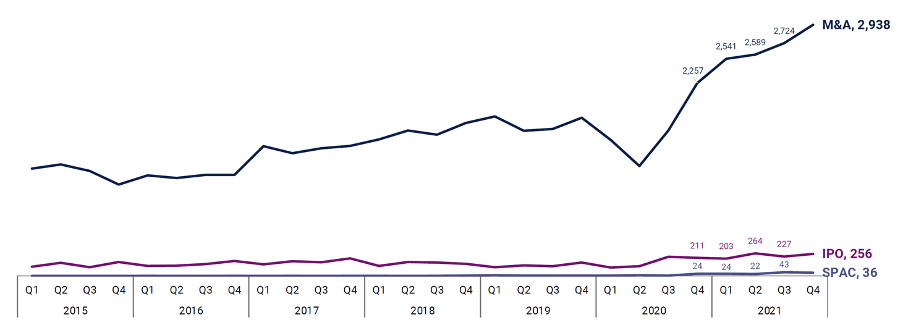

M&A

Digital transformation has become a must-have for companies across all industries, leading to a rise also in M&A activity.

- The number of M&A transactions have gone up six quarters, leading to a record high 2,938 transactions in Q4 2021

- There were over 10,000 M&A transactions in 2021 – also a new record that showed 58% growth compared to 2020

- M&A still dominates as the most typical exit path, but IPOs generate more dollars

Over 10.000 M&A transactions in 2021, 58% growth

Source: CB Insight Report Q4 2021

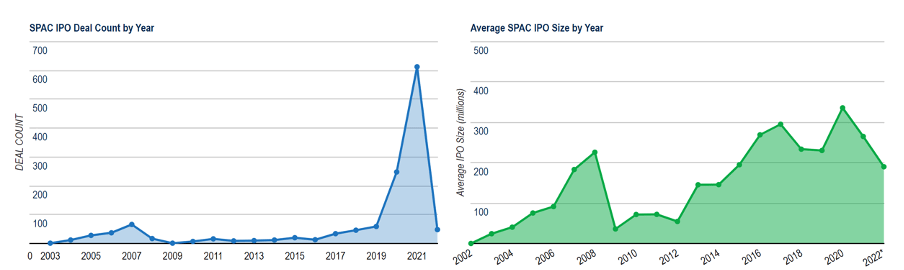

SPAC update – Bonanza no more?

Predictably, the number of SPAC IPOs reached record highs in 2021, increasing to a dizzying 613 from 248 in 2020.

The growth was not stable, though. There were a staggering 298 SPAC IPOs completed in Q1 2021, but the number declined sharply: 60 in Q2, 89 in Q3, and 166 in Q4. The slowdown was caused by increasing SEC scrutiny and more difficult PIPE market conditions.

There were 274 SPAC mergers (the majority in the tech sector) and there are still nearly 570 SPACs with $134 billion looking for mergers within the near future.

However, this SPAC money available does not have a strong direct impact on the VC Exit market as VC-funded companies are more likely to take the traditional IPO route than the faster but more expensive SPAC path. Creating a SPAC is not that expensive per se, but the SPAC teams take typically a hefty price for running the show.

New record: 613 SPAC IPOs in 2021 (248 in 2020)

Source: SPAC Insider, 2022 status at March 06, 2022

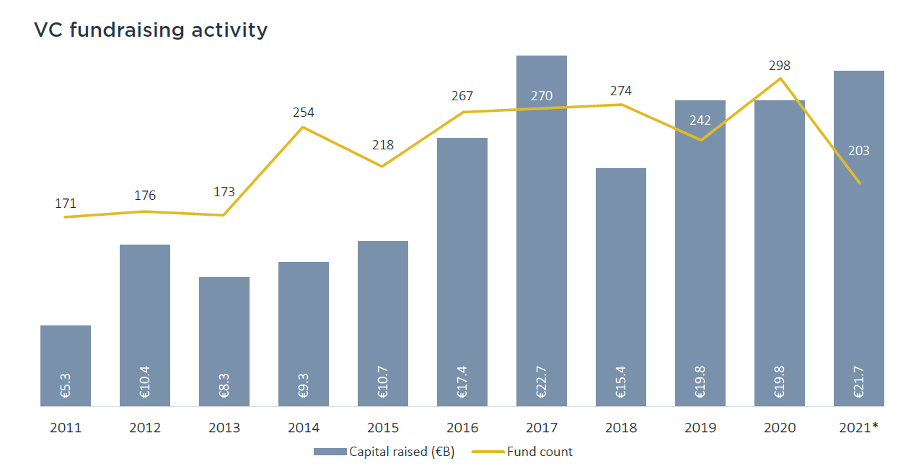

Fundraising in Europe

Unsurprisingly, the bulk of European VC fundraising in 2021 took place in the UK & Ireland, DACH, and France & Benelux ecosystems. These three regions contributed €16.7 billion – equivalent to 76.6% of the aggregate capital raised across Europe.

- European VC funds have raised a fairly steady flow of Euros

- The number of new VC funds was smaller than usual in 2021 – only 203 new funds (the lowest number since 2013) were raised compared to 298 in 2020.

Fundraising in Europe

A steady flow of euros but fewer funds

Source: Pitchbook annual report 2021

Fundraising in the US

In the US the number of new funds raised remained steady (slightly over 700) in 2021. However, multiple large firms were able to close on record-sized funds, leading to nearly $130 billion raised in the US throughout the year. This very large inflow of money might exert upward pressure on the market from funding rates and valuations. Whether the investors exhibit discipline or not is anybody’s guess at this time.

A Quick Note on VC statistics

Overall, VC investment figures are becoming harder and harder to consolidate. On the surface, it appears investments made by VC funds outpaced funds raised by VC funds by a large margin. There are a few notable reasons for this:

- The investment amounts include a significant amount of Corporate VC activity which does not typically show up in the fundraising amounts.

- Furthermore, it appears a lot of PE money flowing into the later stage investments does not show up in the VC fundraising figures.

This variance makes apples-to-apples comparisons a bit difficult and should be kept in mind when comparing the different figures.

In summary: It Was a Very Good Year

The year 2021 turned out to be an exceptionally good year for VC on almost all fronts. This was no surprise: the low interest rates and loose fiscal policy kept stock markets rising and we saw an all-time high for Nasdaq in November of 2021. With the digital transformation progressing along widely on many fronts, the global component shortage or even the rise of Omicron could not spoil the party.

“VC has performed well as an asset class, outperforming Private Equity funds.”

Even though tech companies’ growth and earnings were strong, we started seeing valuation levels that we find unsustainable in the long run.

So what is next – what will the year 2022 bring with it? Stay tuned for our next blog where we offer some analysis and predictions for the coming year, including our analysis of the effect of the elephant in the room – the Ukraine war.

Please, sir, I want some more

Below are some of the key reports and publications we used to source the information above. Enjoy yourselves in getting your fill of additional information!

- CB Insights: State Of Venture 2021 Report

- PitchBook: NVCA Venture Monitor Q4 2021

- PitchBook: European Venture Report 2021

- PitchBook: Global Fund Performance Report

- KPMG: Q4’21 Venture Pulse Report – Global trends

- KPMG: Q4’21 Venture Pulse Report – Europe

- KPMG: Q4’21 Venture Pulse Report – United States

- KPMG: Q4’21 Venture Pulse Report – Asia

- Fenwick: Silicon Valley Venture Capital Survey – Fourth Quarter 2021

- Invest Europe: Annual activity statistics (Some reports for members only)

- Argentum: Number Crunch 2021

- Finnish Venture Capital Association: statistics on Finnish VC & PE activity

- PWC: Global IPO Watch

- EY: 2021 Global IPO Trends

- Silicon Valley Bank: State of the Markets Report H1 2022