Investing after Covid – growth investor playbook

In this installment of the Activist VC blog, we will take a look at the effects of Covid-19 on the investment landscape and where we at Nexit see opportunities going forward.

The evolving investor landscape

After the Covid-19 pandemic hit with full force, I was worried about the markets crashing.

I was wrong.

The unprecedented rate governments are printing money (quantitative easing in fancy terms) has raised the investor sentiment and share prices back to the same stratospheric levels (or even higher in some cases) they started from before the pandemic even though the real economy has been hit hard.

So, there is money. The question is where to put all that moolah as traditional assets are not very attractive:

- The interest rates are likely to stay low, making loans and bonds mostly uninteresting

- Real estate has lost some of its appeal as the rent-paying ability of brick and mortar retailers and restaurants has suffered, and corporations are downscaling their office infrastructure in the face of increasing remote work and layoffs

- Shares appear to be maxed out, at least the big tech stocks – the current multiples do not give much room for further growth

In other words, money is looking for new places to go to. With current public market valuations, returns are difficult to create by just pumping up the valuation multiples. Real returns come from creating new substance, i.e., by concentrating on growing business profitably.

With this backdrop, it is easy to predict that new money will flow into Private Equity (PE) and Venture Capital (VC) investments.

Where are the Growth Opportunities?

Rapid changes in the operating environment always create new business opportunities.

The rate of digitalization before Covid-19 was already fast. The pandemic accelerated the rate of change even further and with a broader impact:

- Consumer and corporate behavior are likely to change significantly in the coming years as we get sensitized to pandemics

- We will see numerous restructurings, pivots, new companies growing rapidly, and big companies disappearing

- Disruption will happen on every level: personal, professional, societal

The value creation opportunities resulting from this development have become massive.

The digitalization of most everything

All aspects of our lives will become increasingly digital, increasingly rapidly:

- Work-life – work from home

- Education – distance learning

- Corporate operations – distributed operations

- Commerce – e-commerce, payments

- Healthcare – telecare

- IT infrastructure – AI, computing power, bandwidth

- Travel, tourism – new innovations needed

These developments have a vital engineering aspect to how they are addressed – we are facing a decade of fast and wide digitalization that offers nearly unlimited opportunities to smart growth companies.

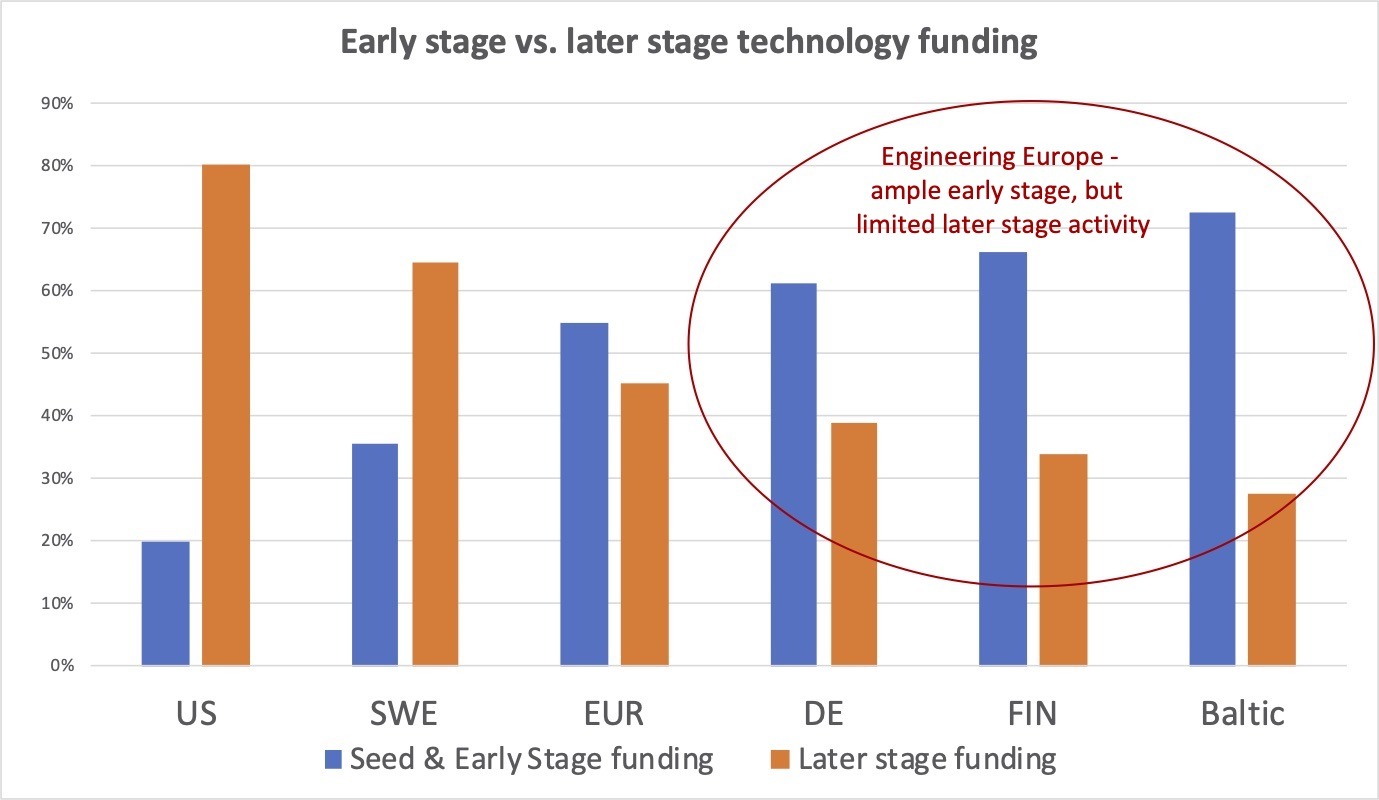

Engineering Europe

Nexit’s primary investment geography is “Engineering Europe”, consisting of Nordics, Central Europe, and the Baltics – an area with a population of 200 million:

- This area offers a very high level of engineering talent combined with comparatively reasonable compensation levels. The proportion of engineers to other college graduates here is higher than elsewhere in the world.

- Most countries within this area have a disproportionally large level of seed/early-stage VC investment activity, but limited tech growth capital.

These factors combine to create plenty of seeds that can become the new high-growth companies in the digitalization space.

Engineering Europe has a very active seed & early-stage market creating a steady flood of high growth investment opportunities for the rapidly digitalizing world – a great opportunity for a technology growth investor. Data: Invest Europe, 10-year average

The ample early-stage funding is great and definitely needed but not enough. To truly fulfill the potential of all these great innovations and startups, a better supply of later-stage growth funding is required. Our next fund will focus on later-stage growth investments and helping the best companies scale up.

And how about the exit environment?

- PE-driven exits of tech firms will become even more common as new money will flow into PE funds

- The transatlantic arbitrage opportunity remains strong: European technology growth companies have lower entry valuations than their US counterparts, but the listed US technology companies will pay top dollar when acquiring new innovation.

At Nexit, we find these opportunities exciting for several reasons. First of all, they are at the core of our investment philosophy. And second of all, we already have a solid track record of taking advantage of them.