ACTIVIST VC BLOG

The Nexit annual VC review: Deep-dive to 2023 Data

March 12, 2024As the calendar turns, so do the gears of venture capital. The data and analyses from 2023 have crystallized, revealing intriguing patterns. In keeping with our annual ritual, we’ve delved into the VC statistics and some related innovation ecosystem reports (you’ll find the list at the end of this article) and distilled the essence for you.

As usual, the analysis is divided into two separate blog posts:

- Part One – Highlights from 2023, a curated collection of noteworthy trends observed

- Part Two – Predictions for 2024, looking to the horizon

Part One is here and Part Two is coming out soon after. Stay tuned as we navigate the currents of innovation and investment!

A Return to Normalcy – or a kind of

The crazy days of Venture Capital (H2/2020-H1/2022) have subsided. During 2023, the market has settled back to levels reminiscent of 2019 across various dimensions.

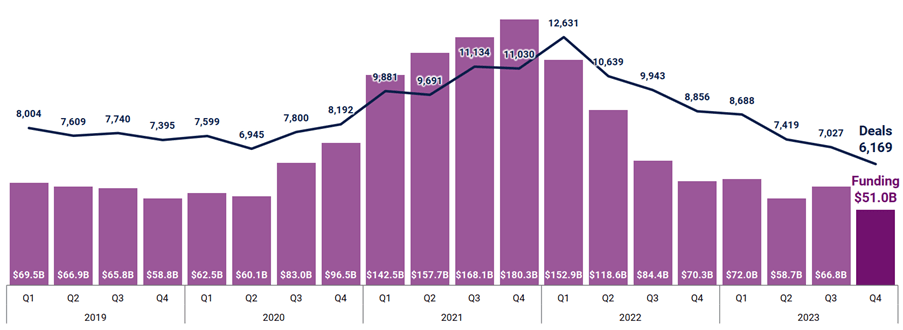

Global quarterly equity funding & deals

Credit: CB Insights Venture Report 2023

Let’s delve into the key numbers from the 2023 VC activity data that reinforce this perspective.

Number of VC Deals

- In 2023, approximately 30,000 VC deals were recorded

- This figure closely mirrors the 31,000 deals observed in 2019

VC Investment Volume

- A total of $250 billion was invested in 2023

- Again, this aligns pretty closely with the $260 billion invested in 2019

And yes, I believe it makes much more sense to compare the 2023 VC activity numbers to the 2019 figures (and skip the crazy days in between) to reveal any meaningful long-term trends. However, it is not – of course – that simple in all the dimensions, as we will see later.

So let’s jump deeper into the 2023 vs 2019 comparison.

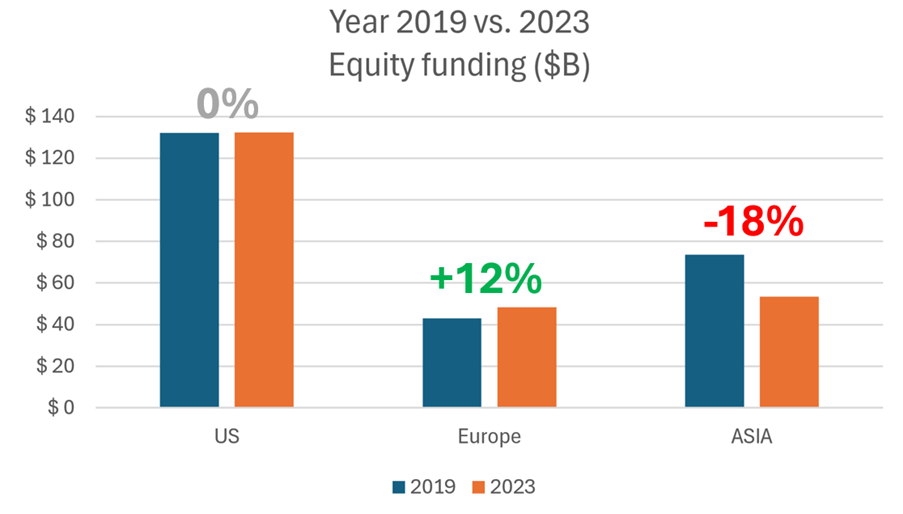

Geographic view

Dollars invested

- In 2023 the US VC dollars invested were back to the 2019 level – with high precision.

- Europe gained 12%, partly because we Europeans are, once again, reacting slowly to the post-crazy-days downturn – just like we did in 2001 and 2009

- Asia was down 18%, partly because the US VC capital has been backtracking from the Chinese market amid the rising political risks

Data source: CB Insights Venture Report 2023

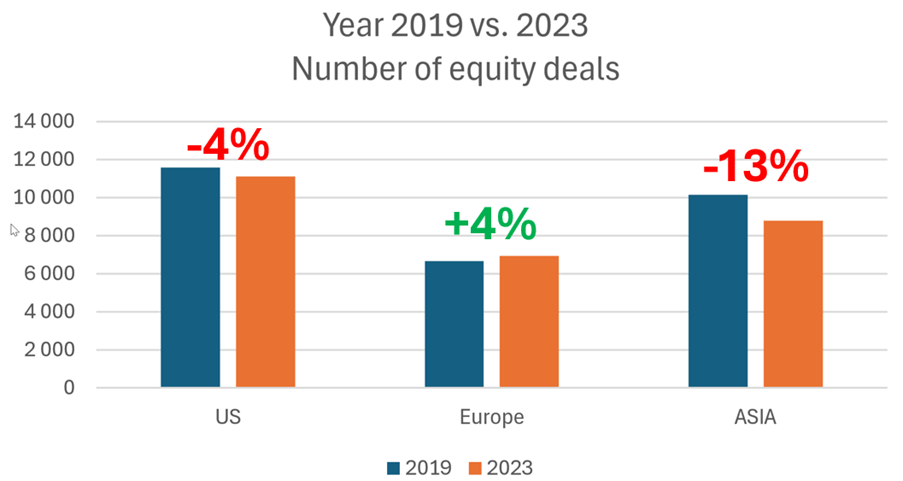

Number of deals

- The number of US VC deals was down 4%, a small margin compared to 2019

- Europe gained 4%, quite flat here as well

- Asia was down 13%, in sync with the lower dollar volume of 2023

Data source: CB Insights Venture Report 2023

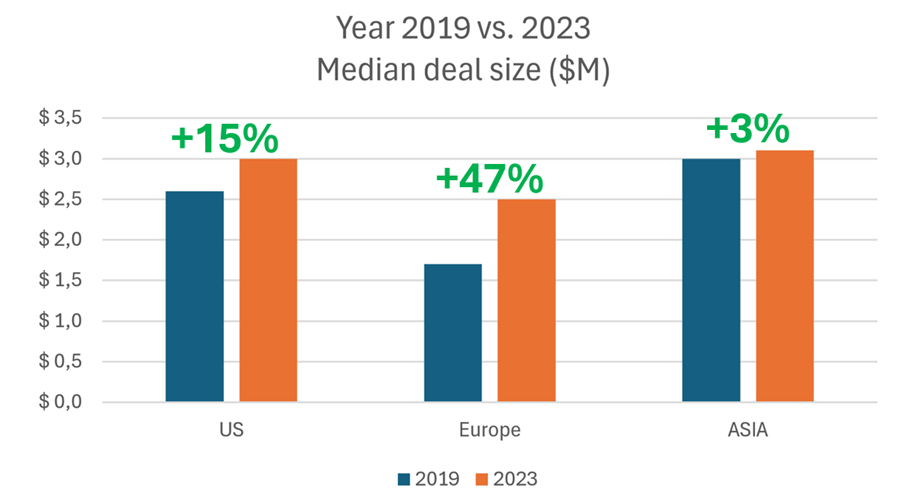

Median deal size

- The US was up by 15%. Our take: the VC fund sizes have grown in the US during the crazy days and larger PE-type investors are also now more active in VC-type deals, both trends pushing the median deal size up.

- Europe +47%, a very Interesting number! I give here two separate explanations, a negative and a positive one:

- 1st: In early 2023, European VCs were once more reacting slowly to the downturn and some of us were still throwing out money like in the crazy days…

- 2nd: Like in the US, the European fund sizes have grown, impacting the deal size.

- I definitely hope that this more competitive median deal size is a lasting and long-term trend as European VC rounds have notably been far smaller compared to the US (or Asian) market – limiting substantially the growth of the European innovation economy

- Asia +3%, nothing special here.

Data source: CB Insights Venture Report 2023

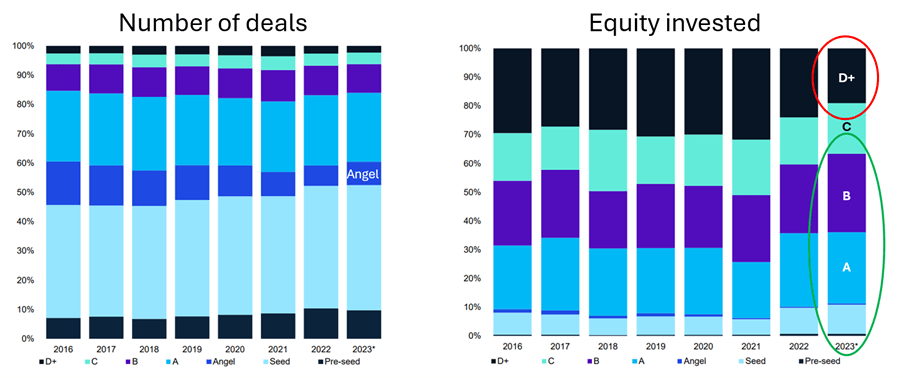

Comparing different development stages

Number of deals

- The split of the deals between different development stages had no major changes

- Amid the strong growth of the VC, PE, and CVC activity (during 2016-2022), the Angel investments lost some position but had a small uptick in 2023

Equity invested

- In 2023 D+rounds received substantially less equity

- Respectively, B rounds and earlier stages received a substantially larger proportion of the invested capital. This trend is directly linked to the lack of the crazy days type of mega deals in 2023. However, the D+ equity investment activity was even below the 2019 level.

Credit: KPMG Venture Pulse Report

Sample active sectors

Based on the recent market activity we picked two topics to dig deeper into: Generative AI and Climate Tech.

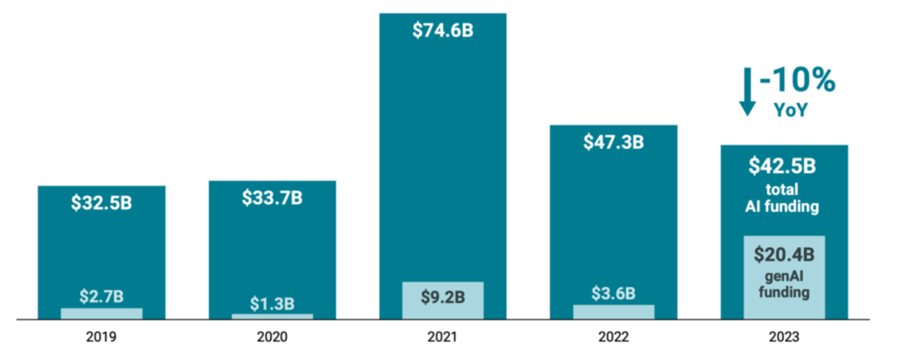

Generative AI

Although AI venture activity slowed down in 2023, Generative AI (GenAI) was a real hot spot:

- GenAI dominated in 2023, attracting 48% of all AI funding (was only 8% in 2022!)

- GenAI was partly driven by massive rounds to LLM (Large Language Model) developers like OpenAI, Anthropic, and Inflection

- The median deal size was also stable at $4.4M, reflecting the overall positive momentum within GenAI – the investment activity was not only made by some extreme mega deals

Data source: CB Insights State of AI Recap 2023

All AI startups raised $42.5B with 2,500 equity rounds:

- The VC dollars invested in all AI deals were down only by 10%: AI took a notably smaller hit than the broader venture funding, which was 42% down in 2023

- AI deal volume decreased by 24%, a bit less than VC in general, where deal volume was down 30%

- The 2,500 AI deals represent, however, the lowest annual deal count since 2017

The US AI VC was up, but Europe and Asia were down

- In 2023, US-based AI startups drew 73% of all AI investments

- The US-based AI startups got 14% more dollars when compared to the previous year

- However, European AI funding was down 29% and Asian AI VC was down a whopping 61%.

AUCH – as a European, I am worried here.

In 2023, AI M&A exits were record high at 317 transactions: the valuations peak as investors and acquirers compete for the deals. Google was the most active investor in AI in Q4’23, backing 9 AI startups. A total of 22 new AI unicorns were created in 2023, down 39% from 2022 – a relatively small decline compared to other sectors. In fintech and digital health, the new unicorns were almost as rare as… …real unicorns.

CB Insights expects genAI startups to maintain positive momentum in 2024, as the genAI boom is far from over. Read more from the CB Insights State of AI 2023 Report.

Climate Tech

As corporations intensify their efforts to meet sustainability targets, innovative climate tech companies are witnessing a surge in demand for their solutions. Despite a 39% drop in equity funding to the sector (amounting to $41 billion in 2023), the number of deals actually increased by 4%, totaling over 2700 transactions. Notably, this growth was fueled by a rise in early-stage deals, which constituted 69% of all climate tech deals in 2023, up from 55% in 2022. The large proportion of early-stage deals reflects the fairly young but rapidly growing Climate Tech scene.

When analyzing Climate Tech startups, I would like to highlight some of the statistical differences compared to mainstream VC funded SaaS companies:

- Investment-hungry hardware elements: Unlike pure SW business models, the majority of Climate Tech startups involve at least some physical and material investments. These hardware elements require additional working capital during the scaling phase. It was not a visible problem while the interest rates were at zero level and money was flying around.

- The physical dimensions might also reduce the scaling speed and efficiency of the business.

- Entrepreneurial Experience: Unlike the SW startup ecosystem with a large pool of seasoned serial entrepreneurs and business-driven experts, the young Climate Tech scene have less entrepreneurial experience in their founder teams, at least here in Northern Europe. Investors need to provide more than just financial support to create success stories.

So – when you set up a Climet Tech fund you need to think differently. In today’s realities, it is difficult to hide the problems by just throwing in more and more equity, instead, the real root causes should be carefully fixed.

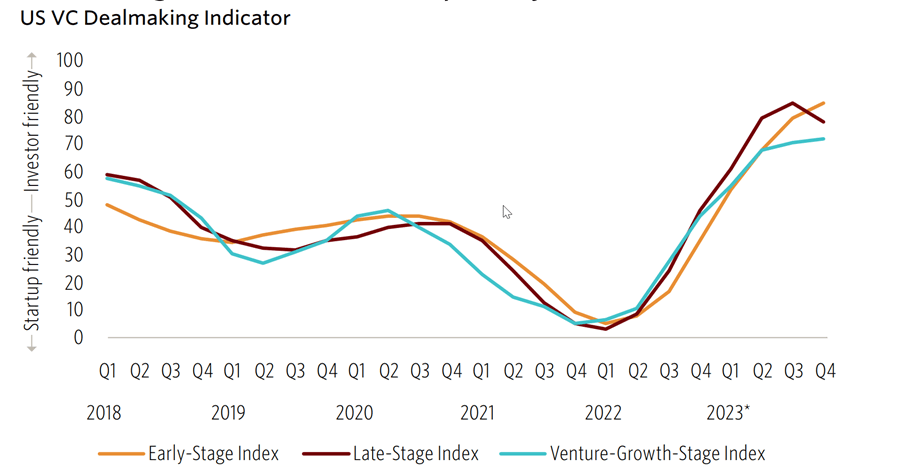

VC deal terms

The VC Crazy Days peak time was at the end of 2021 and the deal terms have changed rapidly since then. crazy days and are now investor-friendly.

Crazy Days status

- The startups were the sole kings of the jungle and VC funds were very flexible just to ensure that they were not left out of the party

- The market also witnessed too many transactions that went fast through without any proper DD process!

- With the zero interest rates, money was cheap, and various potential risk scenarios were valued accordingly (especially anything related to the future funding need)

Current status

- Deal terms are now Investor-friendly (but there has been a significant delay in Europe)

- Flat and down rounds are the new norm

- DDs are done properly, risk awareness is high

In 2008-2009 this swing to the investor-friendly terms was much deeper and faster – the crises hit hard and fast in the US, but the market also recovered quite rapidly. In Europe, the trend came a bit delayed but was substantially prolonged by the euro crisis which was impacting the LP sentiment for several years.

And just to put things in perspective: in 2001-2002 1x liquidation preferences were the norm and 2x-6x multiples were also quite common. So please, stop whining about the current “extreme market conditions”…

Credit: PitchBook NVCA Venture Monitor

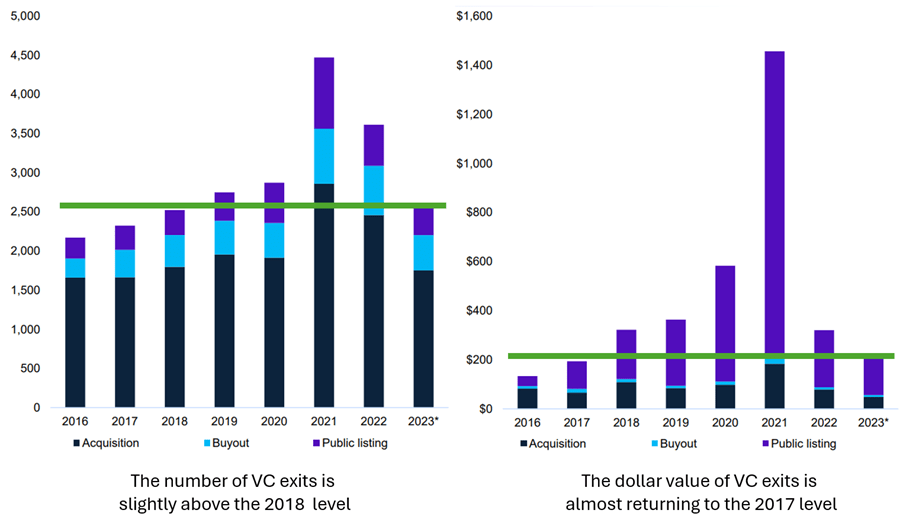

Exit Market

The VC exits in 2023 were also back to pre-crazy-days levels, but we must go a bit further back than just the year 2019:

- The number of VC exits was slightly above the 2018 level

- The dollar value of VC exits was almost returning to the 2017 level

Credit: KPMG Venture Pulse Report

Like always, the US dominated the VC exit market, both on the pure transaction volumes and the high valuation deals. For European VCs the visibility and access to the US exit market is a clear strategic advantage, nothing has changed here.

M&A was still by far the most typical exit path whereas the extremely generous IPO dollars are gone. The share of PE/buyout transactions has seen a fairly steady position in the VC exit playbook, but a clear long-term growth trend can be recognized when looking more than 5 years back.

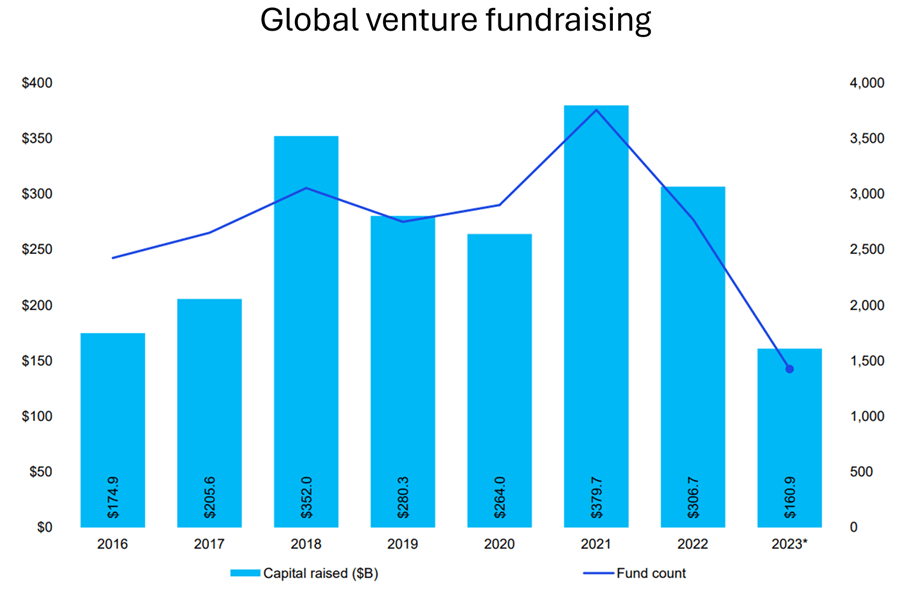

Funds & Fundraising

In 2023 the global VC fundraising was at the lowest level since 2015. The $67B raised by the US VCs is the lowest outcome since 2017 and represents a 60% drop from the $173B raised in 2022, the peak year for fundraising.

Credit: KPMG Venture Pulse Report

The amount of VC dry powder peaked in 2021 and then the market sentiment erosion started and spoiled the merry fundraising parties:

- These dry powder reserves have offered some cushion at least to the lucky VC funds with recently closed large funds.

- Some other VCs (with less lucky timing) are now struggling to survive and protect their portfolio from dilutive down rounds.

- And then there are those fairly new VC funds with a very limited amount of exits and a portfolio full of cash-burning deals picked during the overvalued VC crazy days… (Yes, Nexit was there in 2001 but we survived. And this time we are in a much better position with a small & healthy portfolio and a fairly new fund with dry powder.)

But I am (at least today) fairly optimistic about the near to medium-term VC and LP sentiment. The recent public market recovery in the US has already had a positive impact. And the Europeans typically follow with a 6-12 months delay. Hopefully, there will be no extra delays – like the euro crises after 2008.

More about the market outlook in the next blog post.

Some additional notes from Europe

To create a Europe-centric view of the VC market I highly recommend the State of European Tech 2023 report, from November 2023.

There is both an executive version and also a longer deck with 258 pages.

My three favorite picks from the report:

- The US investor participation is down in Europe (long deck, page 26)

- During difficult times the large VCs tend to emphasize local operations and cut down the international activity. The US VC activity in Europe is now down, but luckily not that much this time (especially when compared to the rapid drops perceived in 2001 or 2009)

- This repeating trend emphasizes the importance of a strong local VC industry to ensure stable growth of the local innovation ecosystem

- Europe is gaining more talent than losing (long deck, page 46)

- Interestingly, more US talent is moving to work in European tech than Europeans moving to join the US tech scene. And further: Europe is a net gainer from all regions excluding Australia

- Is this a longer-lasting trend?

- What do founders want from their VCs? (long deck page 59)

- Notably, the VCs and Founders have very different expectations here

- The clear top item for the Founders was ”Alignment of vision/purpose”, which was regarded as a very low-priority theme for the VCs

- For VCs, the top item was ”Strenght of reputation”, which was again pushed down in the Fonder list

- But there were also some common bullets in the top five of the list: ”Access to relevant network”, ”Chemistry with partner/founder”, and ”Industry expertise”

- This simple study reveals something important for VCs (and LPs) to digest…

- Notably, the VCs and Founders have very different expectations here

In summary: A Return to Normalcy

The year 2023 was a return to normalcy – or at least a kind of:

- Investment activity is back to the 2019 level

- The exit deal count is close to the 2018 level and the exit dollars resemble the year 2017

- Fundraising volumes resemble the ~year 2016 (US 2017 and Europe 2015)

- The deal terms are turning to investor-friendly, almost back to the 2009-2010 level

So what does this mean?

In 2016-2019 the VC industry reported quite positive market conditions in general. And that is exactly what I would say right now as well. Those complaining today have either a short memory or, more likely, have not experienced the real VC Dark Ages (like 2001-2002 or 2009).

Instead:

- The doomsday economic scenarios amid the Silicon Valley Bank collapse failed to materialize

- The Nasdaq has recovered and is today trading at record high levels of over 16.000 points

- New powerful and game-changing innovations are surfacing, creating huge new business opportunities. GenAI is the most visible one today, and more to come.

The sugar coating on top of the VC cake is the deal terms – I would say now is the time to invest. Especially, if the recent rapid recovery of Nasdaq (driven by the magnificent seven) will last long enough to build a new decent exit market momentum for the coming years.

But more about the new trends and market outlook in the next blog post: The Nexit annual VC market review, Part Two – Predictions for 2024

Some data sources used and further reading

Below are some of the key reports and publications we used to source the information above. Enjoy yourselves in getting your fill of additional information!

- CB Insights: State Of Venture 2023 Report

- PitchBook: NVCA Venture Monitor Q4 2023

- PitchBook: European Venture Report 2023

- KPMG: Q4’23 Venture Pulse Report – Global trends

- KPMG: Q4’23 Venture Pulse Report – Europe

- KPMG: Q4’23 Venture Pulse Report – United States

- KPMG: Q4’23 Venture Pulse Report – Asia

- PWC: Global IPO Watch 2023 and outlook for 2024

- EY: Global IPO Trends 2023

- EY: Will venture capital market rebound in 2024 or seek new floor?

- Atomico: State of European Tech 2023 report, November 2023

- Bite Stream Insider: Survival of the fittest – 2023 fundraising lessons for 2024

- J.P.Morgan: The Innovation Economy Outlook

- Fenwick: Silicon Valley Venture Capital Survey – Third Quarter 2023

- Finnish Venture Capital Association: Research and statistics

- Invest Europe: Activity Data

- EIF Operational Plan 2023-2025

- Argentum Statistics

Happy reading!

WE'D LOVE TO HEAR YOUR COMMENTS