ACTIVIST VC BLOG

The Lure of Corporate Venture Capital

December 8, 2017Increasingly often, high tech startups are offered funding by Corporate Venture Capital (CVC) players with seemingly attractive terms. The CVC may also offer synergies, network and other support your business that a regular VC may not bring to the table.

This sounds good, but is there a catch?

Potential mismatch

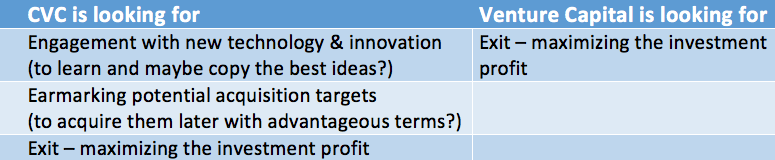

An entrepreneur should keep in mind that CVCs are fundamentally rather different from ordinary VCs. While a normal VC is driven by exit and the increase of the company value, CVC can have different motivations:

Don’t get us wrong: we generally like CVC and we have CVCs in third of our portfolio companies: they can offer a good source of funding and useful additional value.

Aligned interests?

If the CVC investment is syndicated with normal VC money and the investment terms follow industry standards, this kind of arrangement can (and often does) work to mutual benefit. You could also consider adding a competing CVC to the syndicate to minimize the CVC impact: you look much more independent to the industry pundits (and customers) when you are not seen as serving just one master…

However, if the CVC is the lead or sole investor, it can have a negative impact on the growth and exit potential. This is especially true, if the CVC has any right of first refusal type of special rights regarding the exit process.

It also makes sense to check the incentives of the CVC team. If they are ROI-driven like a normal VC, the likelihood of long-term alignment on the path forward is usually good. However, if the incentives are not well aligned with company interests, there is a good possibility of conflicts later on along the road.

Long term partner?

CVC activity is highly cyclical and quite often fickle: the continuity of support from a CVC is dependent upon the strategy, executive management, and financial fortunes of the corporate parent. A startup – which faces daily battles and possibly multiple pivots – should consider whether a CVC can be a patient long-term investor that supports it through thick and thin.

Here, the structure of the CVC can be important: a CVC organized as a plain vanilla fund with reserved funds for future investments and defined time span to spend the money offers a much more stable option than a CVC investing from the parent company’s balance sheet.

Our advice

You should definitely not reject a CVC outright. But in our experience, the following key parameters of the investment and their involvement should be in place:

- The CVC team/entity should have easy-to-understand incentives and motivation that are aligned with yours

- The CVC should not have too dominating role as the shareholder

- Investment terms should follow normal industry standards

- The CVC should not set limitations to your operational plan, future funding roadmap and exit path

- Avoid perpetual or long term special rights or discounts for your products or services

- The CVC should not have a board seat and reporting should be somewhat limited to ensure the integrity of sensitive information.

- The CVC should offer some tangible added value beyond just the money (ideally, there should be a concrete plan in place at investment time)

When these parameters are in place, having a CVC onboard (along with other investors) can be a big plus for your business.

WE'D LOVE TO HEAR YOUR COMMENTS