ACTIVIST VC BLOG

The Great M&A Game

September 27, 2018A brand new study called “Tech Startup M&As 2018” from our good friends at Mind the Bridge shows that the US is still the dominant force in tech startup M&A. As there is a lot of good stuff in the report, we will break down the findings into two blogs:

- In this blog post, we underline the US dominance in tech startup M&A and what the implications are for Nexit and European VC in general

- In the second post, we will take a more detailed look at the M&A balance in different geographies and what Europe could learn from how the US high tech giants operate

The 800-pound gorilla

The study tracked 21,844 trade sale exits of high tech startups since 2010, gathered from CrunchBase data.

US buyers were responsible for 65.8% of these exits while European buyers make 30% of the exits. Buyers from the rest of the world only accounted for 4,2 % of all deals (disclaimer).

The US share of tech startup acquisitions is outsized –

even if we compare it to the GDP: a quarter of the global GDP but two-thirds of acquisitions

Source: World Bank GDP 2017; Tech Startup M&As 2018 Report

Meanwhile in Europe: Rule Britannia

The US is head and shoulders above Europe in M&A, but there are major differences within Europe, as well.

- When we look at where M&A happens in Europe, UK is the undisputed champion

- London had more transactions than the following five European tech hubs combined

- The Nordic countries combined are in second place in selling startups and third place in buy-side transactions

- Germany and France are both are very close to Nordic transaction volumes

- In Finland (the number 2. in the Nordics, half of the Swedish exit volumes), Helsinki is clearly the leading center of M&A activity on both the buy and sell side

The Transatlantic M&A Imbalance

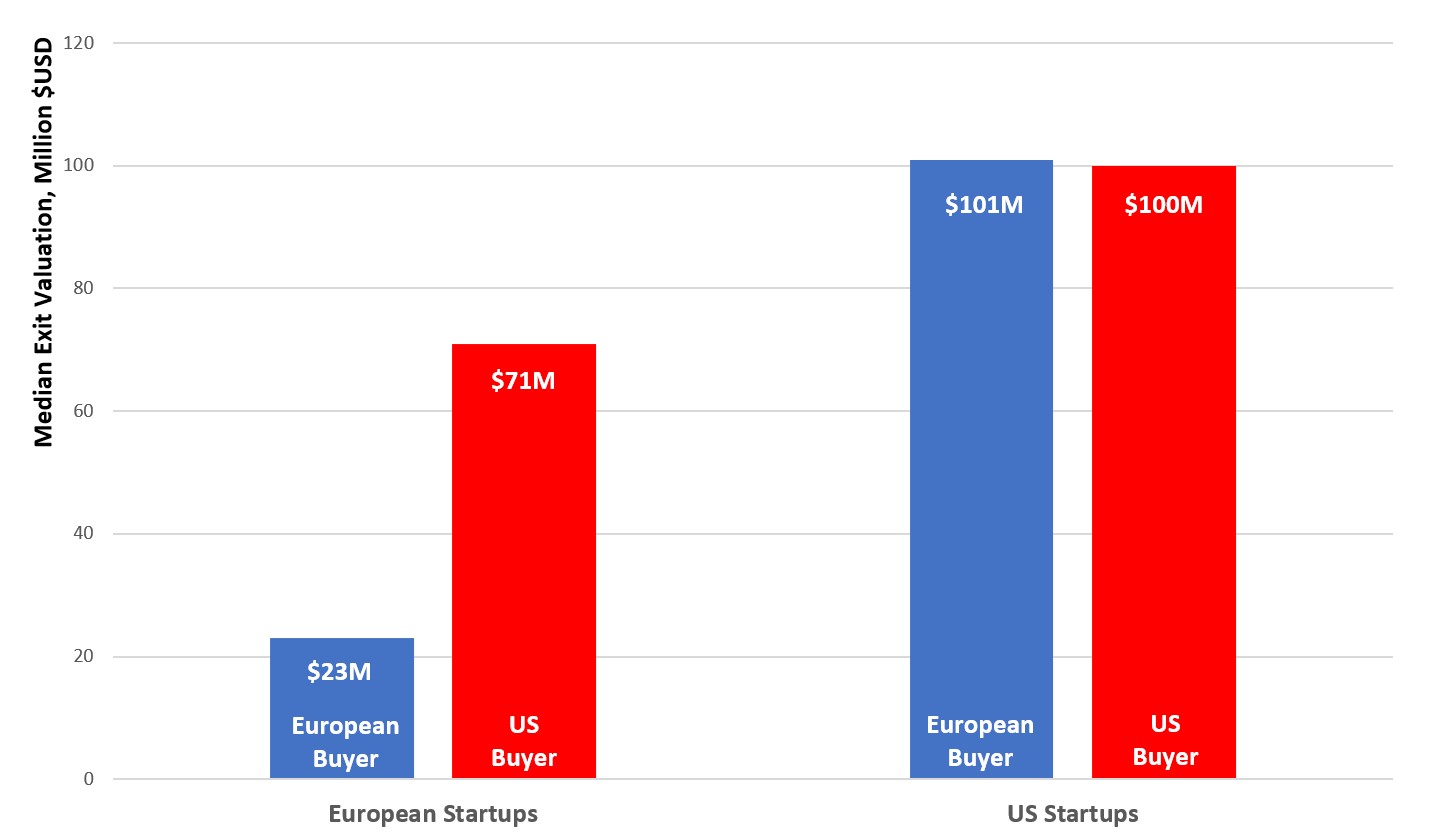

Further analysis of the CrunchBase dataset shows that the vast majority (86%) of M&A happens inside the US and Europe or between the two continents. There is, however, a marked imbalance in these transactions:

- The median exit size of a US startup is roughly $100 million regardless of where the buyer is from.

- When a European startup is sold to Europe, the median deal size is just $23 million.

- However, when a European startup is sold to a US, the median deal size $71 million, over 3x uptick. Ok, this is not quite an apples to apples comparison: the EU startups sold to the US tend to the best of the bunch. But this discrepancy is a strong indicator of the acquisition power and mentality of US Power Buyers.

The 3x median valuation from US buyers compared to European buyers makes a huge difference

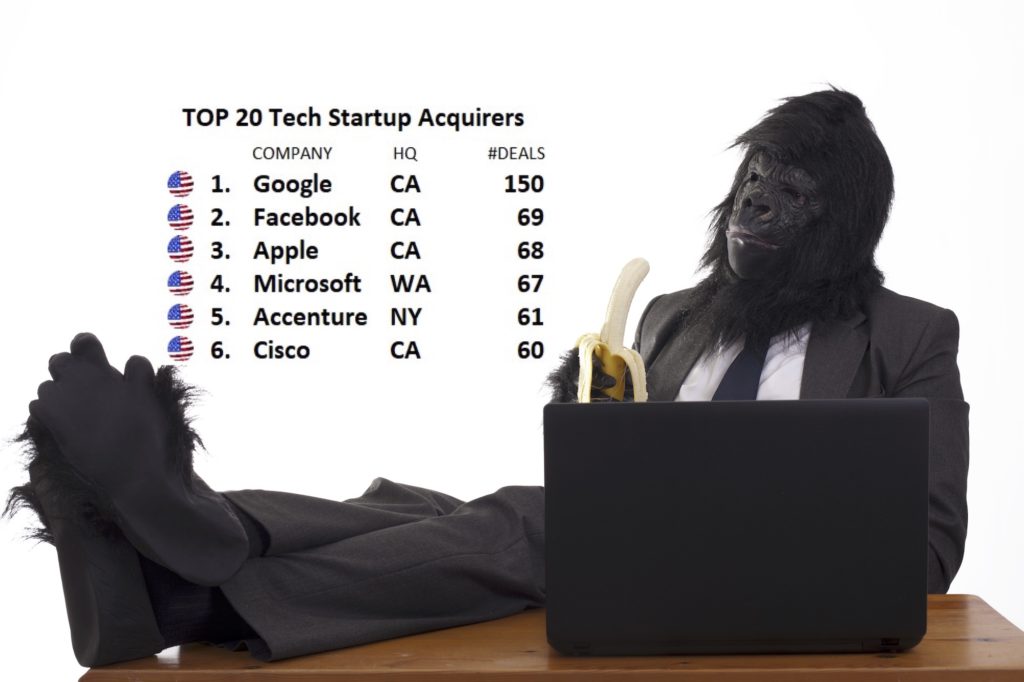

Where are the Power Buyers from?

The message is clear: 18 of the top 20 tech startup acquirers worldwide are from the US, 12 of them from California.

The Power Buyers. Source: Tech Startup M&As 2018 Report.

The only European company cracking the list was #20. While the European VC activity is developing nicely (see this earlier post), we are still definitely laggards in the tech M&A game.

Nexit M&A Takeaways

Our key takeaways from the study combined with our own experiences are as follows:

- M&A is the primary exit route for tech startups

While IPOs are getting a bit more common, they are still few and far between – and the valuations are not better except for some extraordinary cases. - The main buyer cluster is in the US

These power buyers have the market cap, balance sheet, and appetite for growth to acquire companies at a furious pace. It is the Silicon Valley’s recipe for success: buying startups is one of the fastest ways for companies to embrace disruption and keep innovating. - They don’t just buy more companies, they also pay top dollars

The 3x median valuation from US buyers compared to European buyers makes a huge difference for both the entrepreneurs and the VC fund. - Getting on the M&A radar in the US is a necessity

While the US power buyers are shopping for some European startups, they still focus mainly on US companies: 83% of US deals are domestic. Being active and visible in the US market early enough is the way to pop up on the M&A radar of the power buyers.

Proven Solution: The Transatlantic Bridge

One of the key chapters in our playbook since Day 1 has been creating a Transatlantic Bridge for Nordic startups. Being firmly established both in the Nordics and the US, we can effectively help our portfolio companies to succeed in the US market: attract the attention of customers, investors, and potential buyers.

We believe our track record proves this approach is working. More than half of our exits have been to US-based companies, including companies like Google, HP, Akamai, Sybase, and Nvidia.

WE'D LOVE TO HEAR YOUR COMMENTS