ACTIVIST VC BLOG

How to save the startup and VC ecosystem?

March 25, 2020In our previous blog post, we mentioned the COVID-19 pandemic (which, of course, was not a pandemic back then) as a macro threat that may disrupt the venture and startup ecosystem. Unfortunately, we were right to a degree we could not really imagine.

However, there have been startup and VC crises before. In this blog post, we will cover some of Nexit’s experiences from the year 2000 and 2008 crises and how they severely crippled or even destroyed the startup and VC ecosystem.

Tale of Two Crises

Nexit Ventures has fought through two major financial crises: the year 2000 Dotcom Crash and the year 2008 Credit Crunch.

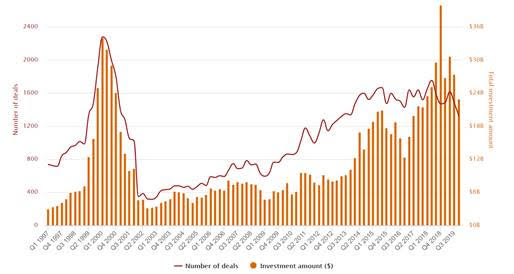

US VC funding from 1997 to 2019, source: PWC MoneyTree

While these crises were quite different in nature, they shared many features:

- All stock markets came crashing down, and the valuations of VC funded companies went down accordingly

- The exit market came to a stop

- The investors behind VC funds (i.e., Limited Partners, LPs) slammed their foot on the brake: the fundraising for new VC funds dried up in an instant

- The Corporate Venture Capital activity dropped to a fraction of the previous level

- To protect their investments, most VC funds moved the focus purely on their existing portfolio to keep at least the most visible (=domestic) investments alive

All in all, there was soon a significant shortage of VC money – and the remaining capital became extremely expensive.

The two crises differed in a significant way, though:

- The challenges of the year 2000 continued for a long time, all the way until early 2003 in the US, and even longer in most of Europe.

- In 2008, most of the problems were over relatively quickly, limiting the level of destruction substantially – at least in the US. (The prolonged euro debt crisis made the VC funding ramp up relatively slow in most of Europe creating many unnecessary startup corpses.)

The Year 2000 Crash

From 2000 to 2003, the impact of the market disturbances in the VC and startup ecosystems grew to a much larger scale. In early 2000 there was an all-time high amount of uninvested VC money around, but it soon disappeared:

- Many VC funds were downsized after a strong push from the LP community – a significant portion of the dry powder just disappeared

- Some fund LPs defaulted, i.e., did not pay up their commitments when the money was called up, diminishing the amount of dry powder even further

- Nearly all Nordic VC funds exited the market in a few years as they ran out of money

- Most US VC funds concentrated on purely on US deals and escaped totally from the European market, making the situation increasingly worse

If an entrepreneur was somehow able to raise additional capital, it meant drastic dilution:

- A rock bottom valuation (at least -50% down round) topped with 2X liquidation preference was a very regular occurrence – even 6X liquidation preferences were often seen

- Alternatively, companies were recapitalized entirely so that the old owners were wiped out

- Some key management team members were usually compensated with new options so that they would stay on board

For the vast majority of entrepreneurs and their VC funded companies, there was simply no way forward. So, vast amounts of entrepreneurial and VC investments in innovation and growth were destroyed.

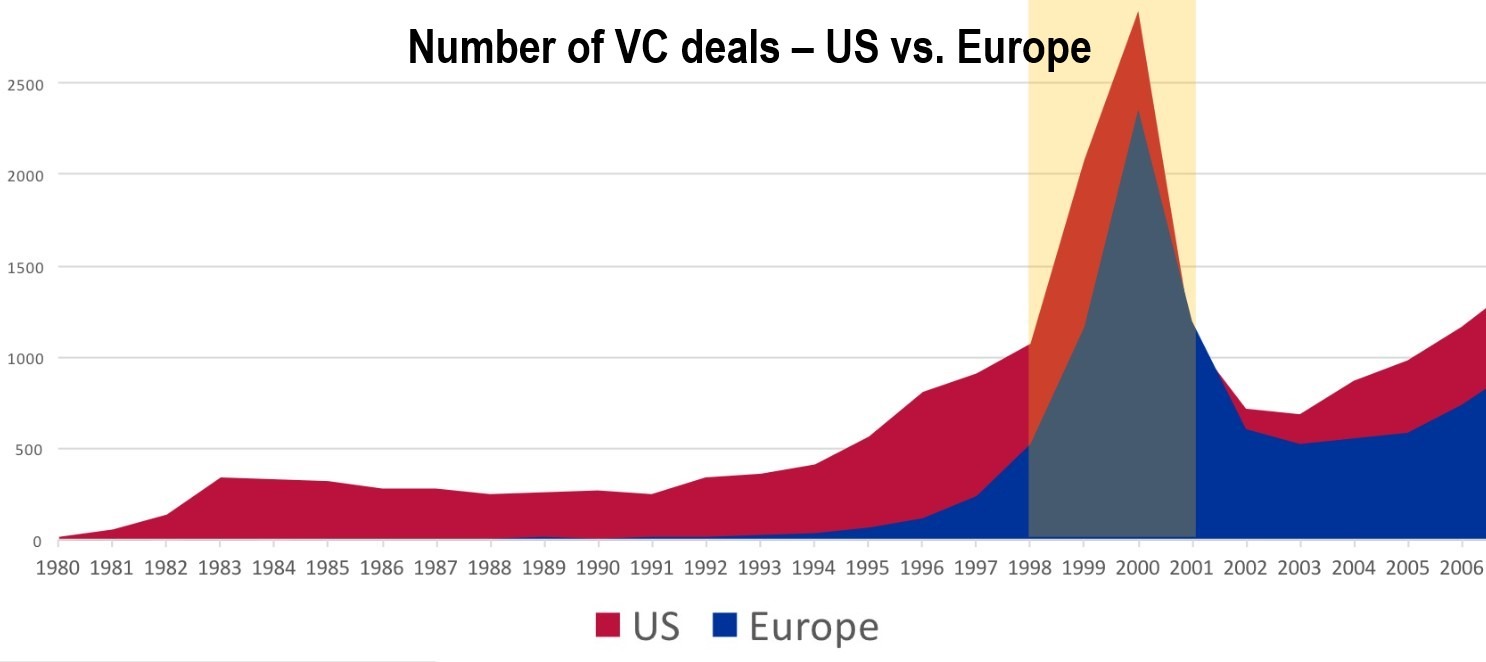

The European view of Dotcom Crash

In 2000, the European VC and startup ecosystem was still very young, thin, and immature. Unlike in the US, the Europeans lacked the steady flow of entrepreneurial VC success stories from the ’80s and ’90s.

After the bubble burst, it took much faith from Europeans to hang with the very distant Silicon Valley entrepreneurial role models. In reality, thousands of European entrepreneurs lost their faith in startups and VC funding for good – a lost generation of entrepreneurial power was generated.

Unlike in the US, the Europeans lacked the steady flow of

entrepreneurial VC success stories from the ’80s and ’90s.

Data: DowJones Venture Source

Nexit’s Approach

During the year 2000 crisis, Nexit took the following approach:

- First, we formed a picture of the portfolio funding needs and exit potential in different scenarios (The worst-case scenario should prepare for a long, L-shape recovery from the crises)

- Next, we calculated the ratio of our full financing responsibility against our remaining capital (In practice, many syndication partners had to drop out, and our responsibility grew)

- Then we reacted early and decisively by dividing our portfolio into three groups:

-

- Ones that should not be funded further

- The ones we could support a little – to help them fight their way to positive cash flow and to somehow survive while waiting for better times

- The most potential ones that we could and should still seriously fund

The result:

- One-third of the portfolio had a happy ending, and we got some very good exits, mainly in the US market. Acquirers included companies like Nvidia, HP, Google, Sybase, etc.

- One-third of the portfolio eked out a living for a few years. About 50% of these companies finally went down, and the other half managed to find a decent exit

- One-third of the portfolio went relatively quickly bankrupt as their funding dried out

The most unfortunate thing for Nexit was that the fund size was reduced by one third, and we lost half of our remaining dry powder. With the new smaller fund, Nexit could not fully defend its position in some high growth companies that required a lot of further funding. Two Nexit investments, in particular, were painfully diluted: Mobile365 (which Sybase acquired for $425M) and Bitfone (which HP acquired for $155M). But regardless of this, Nexit became a positive exception in the year 2000 VC fund vintage and returned a significant share of the capital to its investors.

How to minimize the damage?

It is still too early to say how the COVID-19 crisis will play out: will we hit a prolonged slump á la 2000, or will the ecosystem recover relatively fast like in the US after 2008? Both previous crises were L-shaped in the European venture ecosystem while U-shaped or even V-shaped in the US.

The critical question is: how LPs, VC funds, companies, and government policymakers should work together to make this a short disturbance and avoid the 2000-2003 type of total nuclear winter killing the VC & startup ecosystem?

We are anxious about the potential adverse outcomes:

- loss of entrepreneurial spirit and serial entrepreneurs – the motor for new economic growth and innovation

- serious set-back in VC funding volumes – the fuel for the motor

The tremendous growth opportunities and exciting new technologies are still there. It is up to us all to be wise and decisive and make this a short slump.

Nexit is actively joining relevant discussions and studying related initiatives to be an active part of the rapid startup and VC ecosystem recovery. Be in touch with us if you want to discuss this further.

Stay safe!

Oli kiinnostavaa lukea, kiitos tekstistä ja hyvää jatkoa taistelussa paremman tulevaisuuden puolesta!

A good read.

As entrepreneurs, we have to be honest to ourselves. Whether you have a hotshot team or not, the fact is your business will be non-existent whithin 6 months or less, based on facts. The world economy will change for good. If you’re in a growing scape with your business, I’m happy for you. Fact is, preserve cash, work your strategy, and innovate new. Right now.

Thanks. Really appreciated your past experience and views for today’s situation. This is invaluable at the moment when thinking about our strategies.

Very good analysis. Remembering both crisis the 2000 was much worse. Lack of VC money and VC culture caused many startups to have a bunch of parallel investors. In crisis this caused problems because the strategies of the different investors differed a lot. If a company was funded from somewhere, you could just hear “zip” and the money was gone elsewhere.

It is good to prepare now to the after-corona era. Some preferences and some opportunities are gone, buts some are as good or better than before.