ACTIVIST VC BLOG

The hottest trends in VC

February 16, 2018We have read the latest Venture Capital studies to see the key trends in the market: what is hot and what is not. As a result, we

1. Compiled some of the most interesting trends

2. Added few of our own conclusions and predictions.

The links to the sources we have used are at the bottom of this blog entry. Any interesting reports we are missing? Please let us know.

Strong VC activity on all fronts

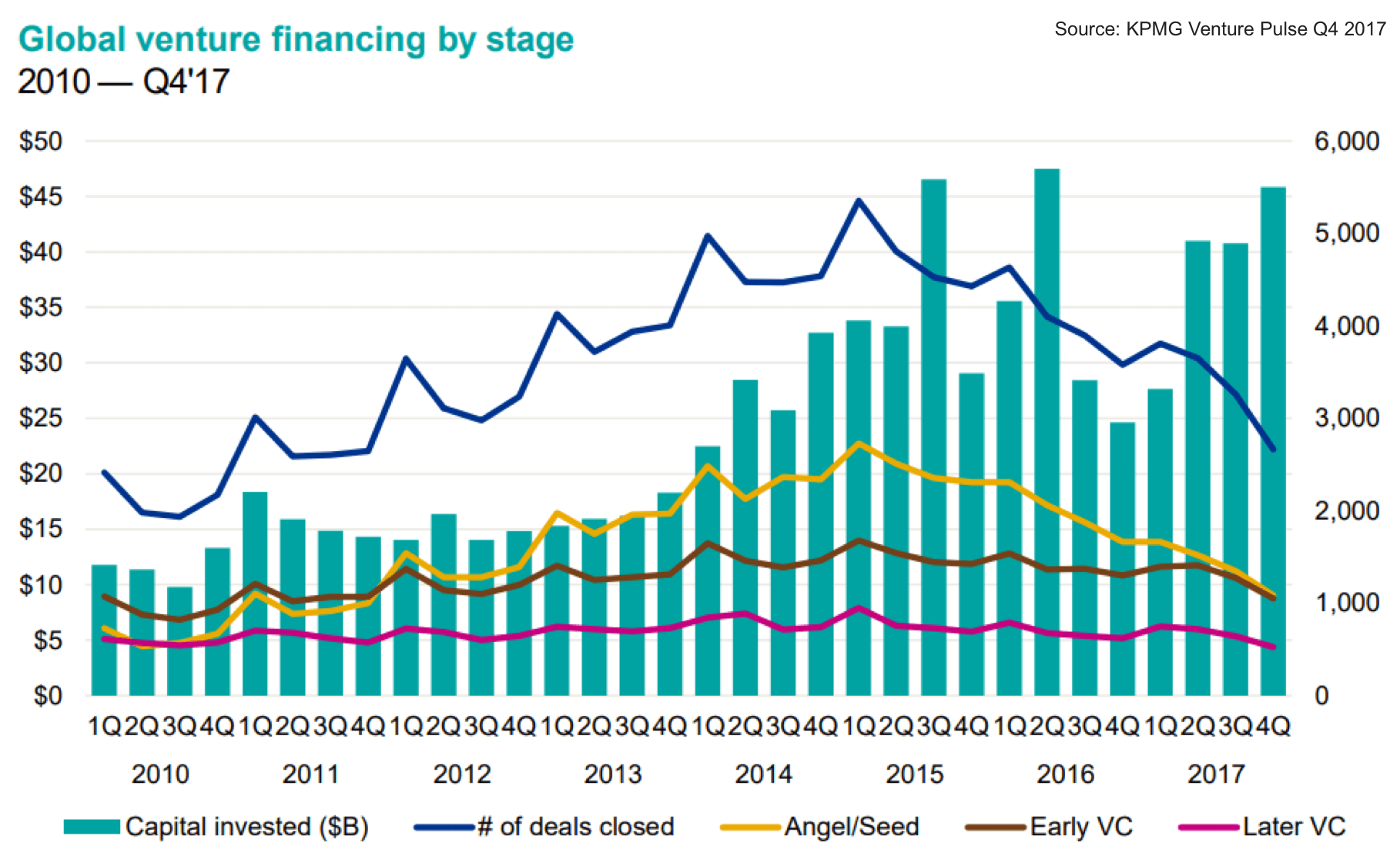

In 2017 the global VC activity reached a record high with over $164 Billion invested, nearly 50% up compared to 2016.

- The US, Europe, and Asia all hit new annual highs for investments

- Corporate Venture Capital activity reached a new high and CVCs were involved in nearly 20% of all VC deals

- European market got more competition: US VCs participated in 17.1% of European deals, up from 13% in 2016

Funding volume is up but number of deals is down

The dollar amounts are up…

- An increasing number of $100+ Million megarounds, with 109 such rounds in the US

- Six investments over $1 Billion during Q4 alone

- The two largest of these were not in the US but in China

…but the number of deals is down

Even with the record amount invested, the total number of VC deals (11,000) was significantly down from 2016

- Less first round investments, back to the lo levels of 2010

- Dollars invested in first rounds has decreased by 30% since 2015

- France was a rare exception having growth of early stage deals

Entrepreneur friendly terms

- Deal sizes and valuations rose in all stages

- Europe had 70% up-round deals, US was even higher at 79% – both well above the long term averages

- Investment terms remained very entrepreneur friendly

Exit market is active

- Global IPO volumes highest for a decade, 48% up from 2016

- IPO boom continued in Nordic, Stockholm alone had 79 IPOs

- M&A transactions: valuations high but amount of deals mediocre

- Buyout exits were high: record year both in dollars and deals

Trends in 2018

Artificial Intelligence had a monster year in 2017, with over $1 Billion invested in every quarter of last year in the US alone. The global investment in AI ($12 Billion) was 100% above the 2016 number. And the AI juggernaut is not going to slow down in 2018 with AI being increasingly applied across sectors.

Automotive technology (and especially technologies related to self-driving cars) are likely to continue to be a hot area and attract a great deal of money in 2018.

And while cryptocurrencies are viewed with some suspicion, the underlying blockchain technology will remain relevant and be increasingly utilized in protecting digital assets and transactions across digitally disrupted industries.

While VR might be losing some of its steam, AR (augmented reality) seems to be surging ahead. Both big corporates and innovative startups are innovating in this sector and AR seems increasingly likely to start hitting the mainstream and attracting a lot of investments.

Nexit’s take

We would like to offer four predictions based on our experience and the way we look at the market and technology landscape:

- We continue to believe in the digital disruption and the enabling technologies behind it. This is an extremely important and long-lasting trend that will keep growing in 2018 and far beyond impacting heavily all industries around the globe. A great source of opportunities for entrepreneurs (and VC funds).

- Corporate Venture Capital is likely to repeat its past patterns: the excitement in CVC will subside when the general market sentiment start cooling down. The big waves of corporate venture activity (late 1960s, mid-1980s, late 1990s) correspond with the booms in VC investments. And now we have another high activity period ongoing – both in VC and CVC.

- Our bet on the ICO market: the ICO bubble will – if not burst – at least deflate during 2018. The underlying Blockchain technology, however, will keep developing. We believe ICOs do not go away as a funding mechanism but that they will develop into a safer and more consumer-friendly crowdfunding vehicle. Legislation and regulation controlling ICOs will undoubtedly get tighter.

- Reward-based Crowdfunding is likely to keep developing in a stable and positive manner and can have even stronger synergies with VC funding.

Sources and further reading

Below please find the principal sources used in researching this blog post.

- KPMG Venture Pulse: Global and regional trends in VC

- PwC MoneyTree: Detailed US VC activity since 1995

- PitchBook-NVCA Venture Monitor: US VC ecosystem

- Fenwick & West VC Survey: VC deal terms in the Silicon Valley

- Invest Europe activity statistics: Pan european VC & PE activity (many of the reports are for members only)

- Argentum Insight: Nordic VC & PE activity

- FVCA statistics: Finnish VC & PE activity

- PwC IPO Watch: IPO statistics

- Silicon Valley Bank: US view on the innovation economy

- State Science and Technology Institute: VC trends to watch

- Kleiner Perkins Internet Trends: Mary Meekers Internet Trends

- McKinsey Global Institute: Digital Disruption in Europe

WE'D LOVE TO HEAR YOUR COMMENTS