ACTIVIST VC BLOG

The hottest VC trends of 2019

March 18, 2019One of our most popular posts last year was our review of the hottest VC trends of 2018. So, without further ado, here is an updated version for 2019.

Similarly to last year, we reviewed a ton of VC and startup related reports and studies and:

1. Compiled some of the most interesting trends

2. Added some of our own conclusions and predictions.

Strong VC activity continued

In 2018, we saw another 50% growth in VC activity, with a staggering total amount of $255 Billion invested:

- Companies residing in the Americas still dominate the global scene with 53% of the total investments received with $136 Billion

- Companies in Asia Pacific raised funding actively and investment activity grew to over $90 Billion, but the global share declined slightly because of the super-fast growth in Americas

- VC funding to European companies grew only slightly to just over $24 Billion, but the global share of European VC dropped to under 10% of the global investment activity.

Despite the record amount of funding, the global number of deals declined for the third year in a row – the focus was in large late-stage deals:

- There were nearly 150 funding rounds with a post-money valuation of $1 Billion or more, with Ant Financial (China, $14B) and Juul (US, $12.8B) leading the way

- Especially the large, global VC funds were acting more and more like Private Equity players and concentrated on very large later-stage deals

- In total, there are now more than 300 private unicorn companies globally – it can be said that in many cases IPOs are being replaced with mega rounds that include exits by the early investors, while late-stage investors keep companies private for a longer time

The European perspective

- Europe and the Nordic region are producing a fair amount of unicorns but they are primarily funded with US-based investments. Nordics and Baltics are the clear sources of late-stage growth, with fifteen 1B USD+ exits, representing more than half of the European unicorns.

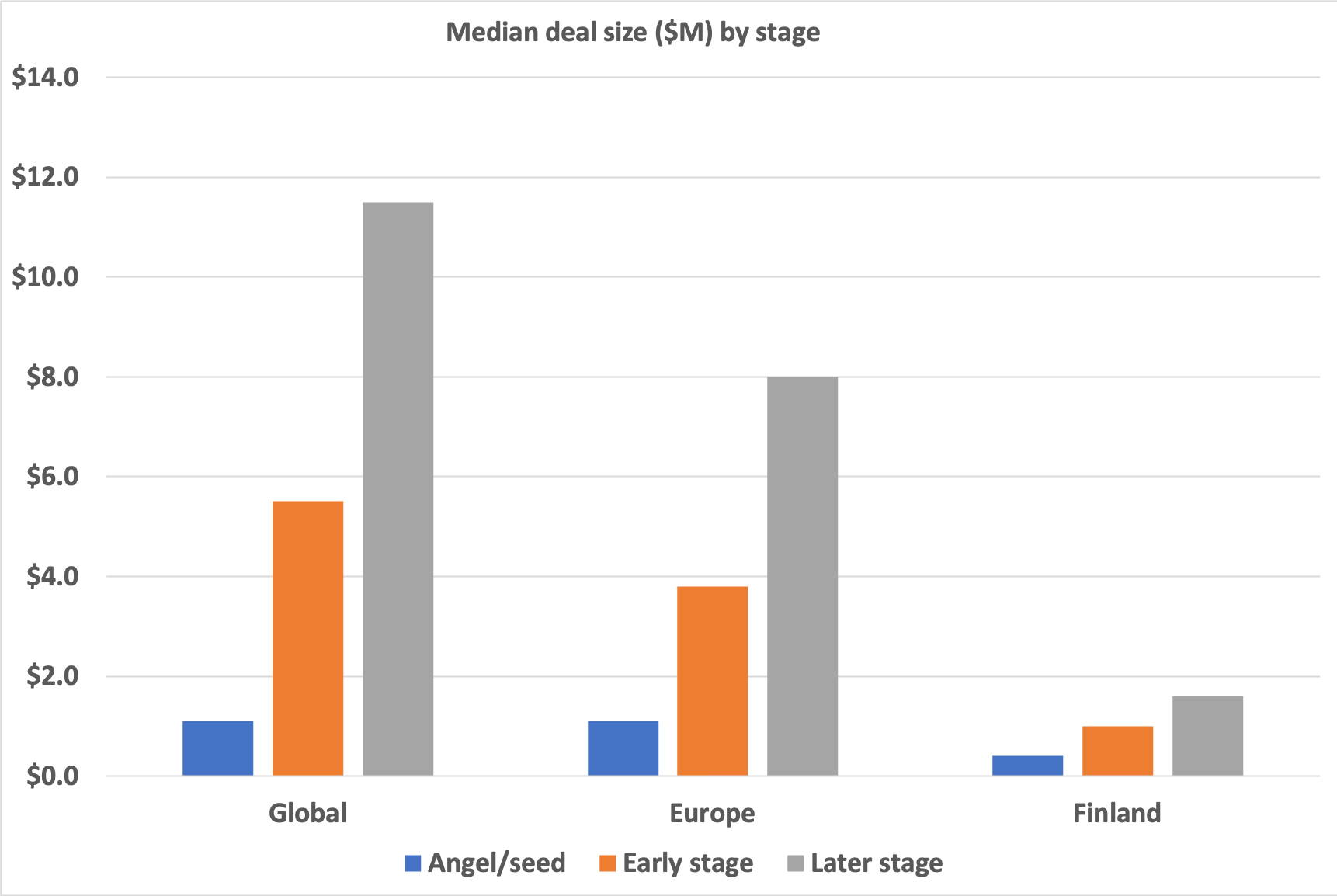

- The median deal size in Europe took a big leap to the right direction but is still clearly behind the rest of the world

- The Nordics – and especially Finland – are, unfortunately, clearly behind the rest of Europe when we look at deal sizes. See the graph below for details:

Finland lags badly behind in median deal sizes

(KPMG Venture Pulse Q42018 report and for

Finland estimates from the Invest Europe EDC database 2017)

Corporate Venture Capital

- The share of Corporate Venture Capital kept growing and CVCs were involved in over 20% of all VC deals

- However, there was a sharp decline in CVC participation in Q3 an Q4, most likely due to the stock market correction

Funding volume is up but the number of deals is down – again

Emerging markets are stepping up

- China is the undisputed king of VC in APAC but companies from Singapore (Grab), Indonesia (Tokopedia), and India (Swiggy) raised $1B+ rounds

- Large rounds are happening in outside of APAC, as well. The Brazilian digital content provider Moviles raised a $500M+ round in Q4

- Companies from emerging economies such as Brazil, Colombia, Mexico, India, Malaysia, and Indonesia attracted well over $8 billion in investment

Valuations and up rounds still growing

- Deal sizes and valuations rose in all stages

- The portion of up rounds was further up, reaching nearly 80% with down rounds amounting to just over 10%

- Investment terms remained very entrepreneur-friendly

A strong exit market, affected in Q4 by the stock market correction

- The total exit market (including both M&A and IPOs) set an easy all-time-high with more than $300B in exits. This was more than double than the exit volume of the already robust 2017

- Exit activity was particularly high in Q2 and Q3, but came down in Q4 amid the global stock market correction

- The number of M&A transactions was lower than any time since 2010 but the dollar amount hit a new record at nearly $100B

Fundraising continues to be strong

- While the number of new VC funds declined somewhat, the total dollar amount raised hit a new high at $78 Billion

- While the share of first-time funds grew somewhat, follow-on funds still amounted to over 80% of new funds

- Both the number and relative share of $100M+ funds grew clearly compared to earlier years

- However, in Finland, only one fund of more (ever so slightly) than 100 Meur has been raised

Nexit’s take on VC trends

We would like to offer four predictions based on our experience and the way we look at the market and technology landscape:

- 2019 will be an exciting and unpredictable year in the VC industry. While 2018 was a record year, the Q4 stock market correction did impact the market and volatility grew. Stock markets are still nervous and the political situation (e.g. US vs. China, Brexit, India vs. Pakistan) is more unsettled than it was at the beginning of 2018.

- As we predicted last year, Corporate Venture Capital did cool down with the H2 market correction (albeit the overall CVC share grew). While the levels are still high, continued growth is dependent on how the stock markets recover during the year.

- We predicted that the ICO market would cool down during 2018 and this did indeed occur. As we said last year, we believe ICOs do not go away as a funding mechanism but that they will develop into a safer and more consumer-friendly crowdfunding vehicle. Legislation and regulation controlling ICOs will undoubtedly get tighter.

- We continue to believe in the digital disruption and the enabling technologies behind it. This is an extremely important and long-lasting trend that will keep growing in 2019 and far beyond, impacting heavily all industries around the globe. This is a great source of opportunities for entrepreneurs (and VC funds).

Digital Disruption is an on-going, long-term, global megatrend

We at Nexit believe that the next long-term productivity-enhancing set of technologies have emerged to transform business-to-business operations and various industrial processes.

- Machine Learning based technologies augment scalable operating models, bring better predictability and faster, a more agile way for companies to react to dynamic changes in their operating environment.

- AI-based advanced hardware platforms and data-driven software stacks help companies to enable or exploit new business opportunities.

A perfect storm with the current available talent, readily available and affordable computing capacity, and the ability and the instrumentation to capture relevant industrial data from the business and product operations is here today. According to the World Economic Forum, AI-generated digital dividend will exceed 100 Trillion dollars of value to societies and business, and industrial actors can capture nearly 13 Trillion USD of value from AI by 2030.

PriceWaterhouseCoopers, McKinsey & Co., and World Economic Forum all estimate that global GDP could be 14% to 16% cumulatively higher (13-16 trillion USD) in 2030, due to the adoption of applied artificial intelligence technologies across different industries. McKinsey further estimates that up to 70% of the companies have adopted AI-based technologies by then– but not fully.

Unfortunately, Europe’s share of investments in applied artificial intelligence technologies is only 9% of the global investments (mimicking the modest share of the overall VC activity in the region). Other factors slowing down adoption and the use of machine learning as a competitive advantage in Europe, are relatively conservative corporate cultures in European corporations and lack of adoption in data-driven strategic decision making.

We believe that corporations in Europe will have to start increasing adoption of the applied AI technologies, through acquisitions of AI-based products and services and potentially incorporating startups via M&A to their core future business operations.

European share of the M&A deal flow has been around 30% of the global M&A deal flow in terms of cases, but only 18% in terms of dollar value. To speed up the adoption and to create competitive advantages, European corporations could increase the inflow of new ideas, technologies, and talent via faster and more aggressive investment and M&A activity.

Northern European applied AI startup ecosystem has never looked stronger in terms of quality and opportunities to invest in our opinion. Nexit Ventures is executing our mission to invest Nordic growth capital sustainably and profitably to strengthen the digital disruptor’s positive impact on society.

Sources and further reading

Below please find some principal sources used in researching this blog post and other good sources of venture industry information.

- KPMG Venture Pulse: Global and regional trends in VC

- PwC MoneyTree: Detailed US VC activity since 1995

- PitchBook-NVCA Venture Monitor: US VC ecosystem

- Fenwick & West VC Survey: VC deal terms in the Silicon Valley

- Invest Europe activity statistics: Pan European VC & PE activity (many of the reports are for members only)

- Argentum Insight: Nordic VC & PE activity

- FVCA statistics: Finnish VC & PE activity

- PwC IPO Watch: IPO statistics

- Silicon Valley Bank: US view on the innovation economy

- CB Insights: Game Changing Startups 2019

- World Economic Forum: $100 Trillion by 2025: the Digital Dividend for Society and Business

- McKinsey: Notes from the AI frontier – Modeling the impact of AI on the world economy

- PWC: AI to drive GDP gains of $15.7 trillion with productivity, personalization improvements

- World Economic Forum: The global economy will be $16 trillion bigger by 2030 thanks to AI

Very interesting, thank you for sharing!